The sheet metal fabrication industry is going through one of those rare periods where almost everything’s pointing in the right direction. Electric vehicle programs are ramping up. Infrastructure spending is real. Companies are serious about reshoring. And the demand for precision fabrication keeps growing across industries we’ve been serving for decades.

If you’re evaluating fabrication partners or trying to understand where the industry’s headed, here’s what the data actually shows—and what it means for your sourcing strategy.

TL;DR: Every major end-use sector—automotive, aerospace, electronics, construction—is expanding its dependence on advanced sheet metal fabrication. New 2025 forecasts place the global fabrication services market at $17–22B today and $30–33B by the early 2030s, with nearshoring, EV manufacturing, and automation driving sustained demand. As demand increases across multiple segments simultaneously, buyers should expect capacity to tighten and lead times to fluctuate more sharply, especially for advanced materials or certified work.

The Market Numbers: What They Tell Us (and What They Don’t)

Let’s start with the headline figures. The North American sheet metal fabrication equipment market hit $7.7 billion in 2023 and is tracking toward $11.9 billion by 2030—that’s 6.4% compound annual growth. The U.S. holds about 75% of that market.

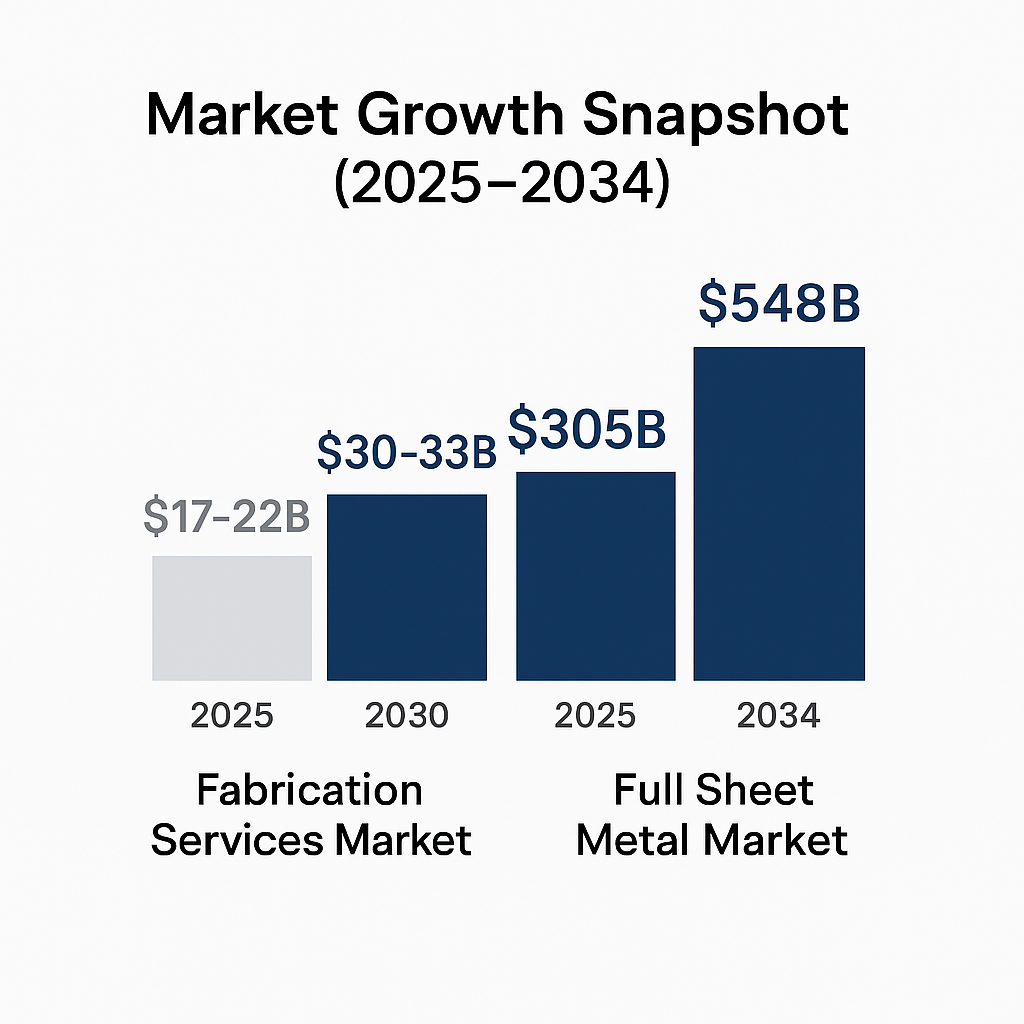

More relevant for 2025 planning, the global fabrication services market sits around $17–22 billion depending on whose methodology you trust, with projections climbing to $30–33 billion by the early 2030s. Different research firms use different scope definitions, but they all agree on the direction: steady, sustained growth through this decade.

The broader sheet metal market—everything from raw materials to finished products—is even larger, estimated at $354 billion in 2025 and climbing toward $548 billion by 2034.

Why This Growth Wave Is Different

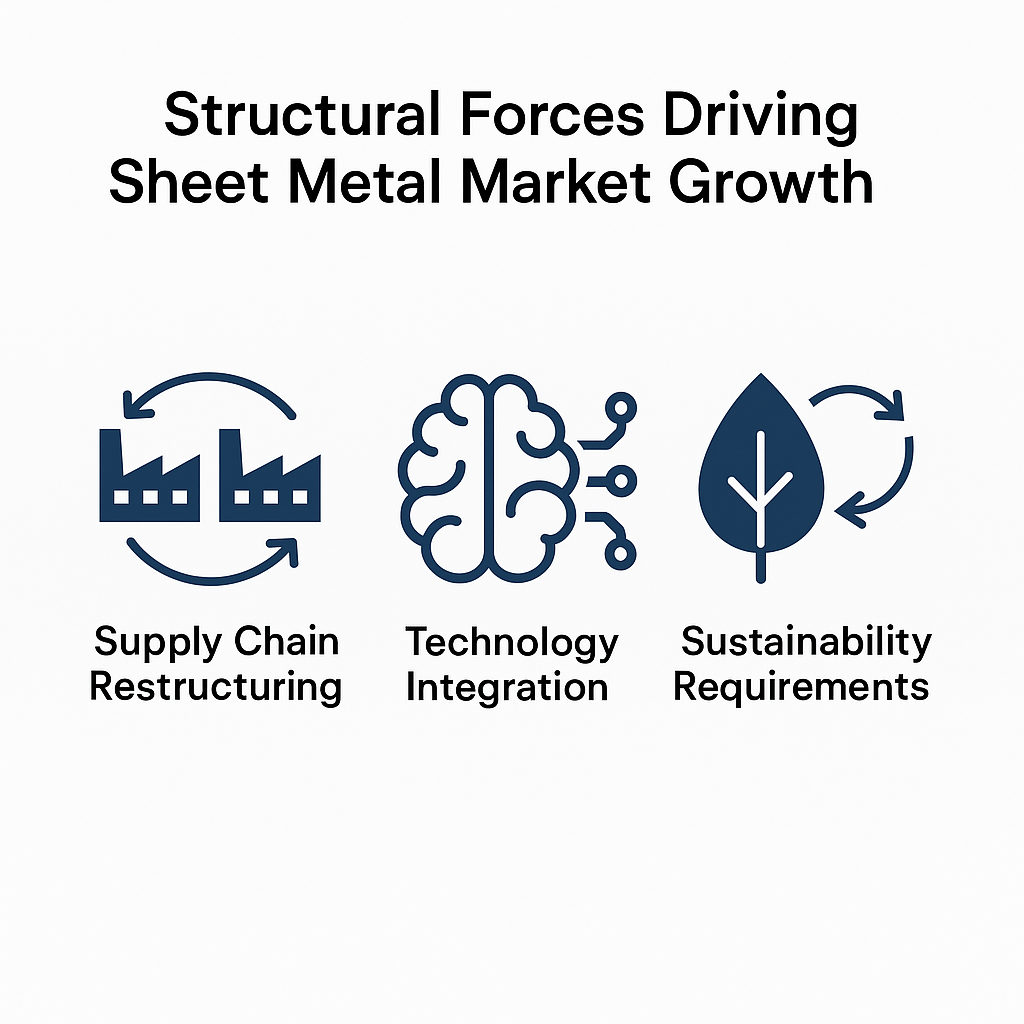

What’s driving this? Three structural forces that aren’t going away:

Supply chain restructuring. Nearshoring isn’t a trend anymore—it’s how companies operate now. After the disruptions of the past few years, buyers want fabrication partners they can actually visit, with backup capacity they can verify.

Technology integration. Fiber lasers, robotic welding, and modern inspection/measurement systems aren’t experimental anymore. They’re baseline expectations for precision work. Automation and robotics adoption in metalworking and fabrication continues to ramp up. In the U.S. alone, approximately 101,700 industrial robots were deployed in metal fabrication operations in 2023, and projections suggest this number will more than triple by 2030—a substantial acceleration across the industry.

Sustainability requirements. More RFPs include carbon footprint questions. More buyers care about waste reduction and energy efficiency. It’s becoming a competitive differentiator.

Industry Segment Breakdown: Where the Real Demand Lives

Automotive & Transportation: The EV Effect Is Real

Automotive has always been a major fabrication customer, but the shift to electric vehicles is changing what they need and how much of it. EV programs require:

- Lightweight aluminum components for range optimization

- High-strength steel alloys (AHSS/UHSS) for structural and crash safety systems

- Battery enclosures and thermal management assemblies that didn’t exist in ICE vehicles

The Grand View Research analysis identifies automotive as one of the core end-use markets driving both equipment purchases and fabrication services growth. Commercial vehicles and aftermarket programs sustain additional demand beyond the EV wave.

Aerospace & Defense: Precision Work at Scale

Aerospace and defense fabrication isn’t high-volume, but it demands capabilities most shops can’t deliver: tight tolerances, certified processes, full material traceability, and rigorous documentation. Market forecasts consistently cite aerospace as a driver of advanced fabrication equipment adoption—CNC machining, laser cutting systems, and robotic forming.

If you’re in this space, you already know the qualifiers narrow fast. ISO 9001:2015 certification is table stakes. AS9100 and ITAR open more doors.

Construction & Infrastructure: The Long-Duration Driver

Construction represents one of the largest global end-use segments for sheet metal—HVAC systems, architectural cladding, structural components, and utility enclosures. Industry studies peg construction as a top sector fueling sheet metal growth through 2030.

Federal infrastructure programs and renewable energy buildout add durable long-term demand. These projects have long timelines and predictable volumes, which matters when you’re planning capacity investments.

Electronics & Telecommunications: Faster Growth Than Most Realize

Data centers, 5G infrastructure, and electronics manufacturing create steady demand for precision enclosures, racks, cable management structures, and thermal systems. Market forecasts identify electronics as a growing contributor to overall fabrication expansion.

The electronics sector growth we’re seeing isn’t speculative—it’s tied to physical infrastructure buildout that’s already funded and in progress.

Material Trends: What’s Actually Being Specified

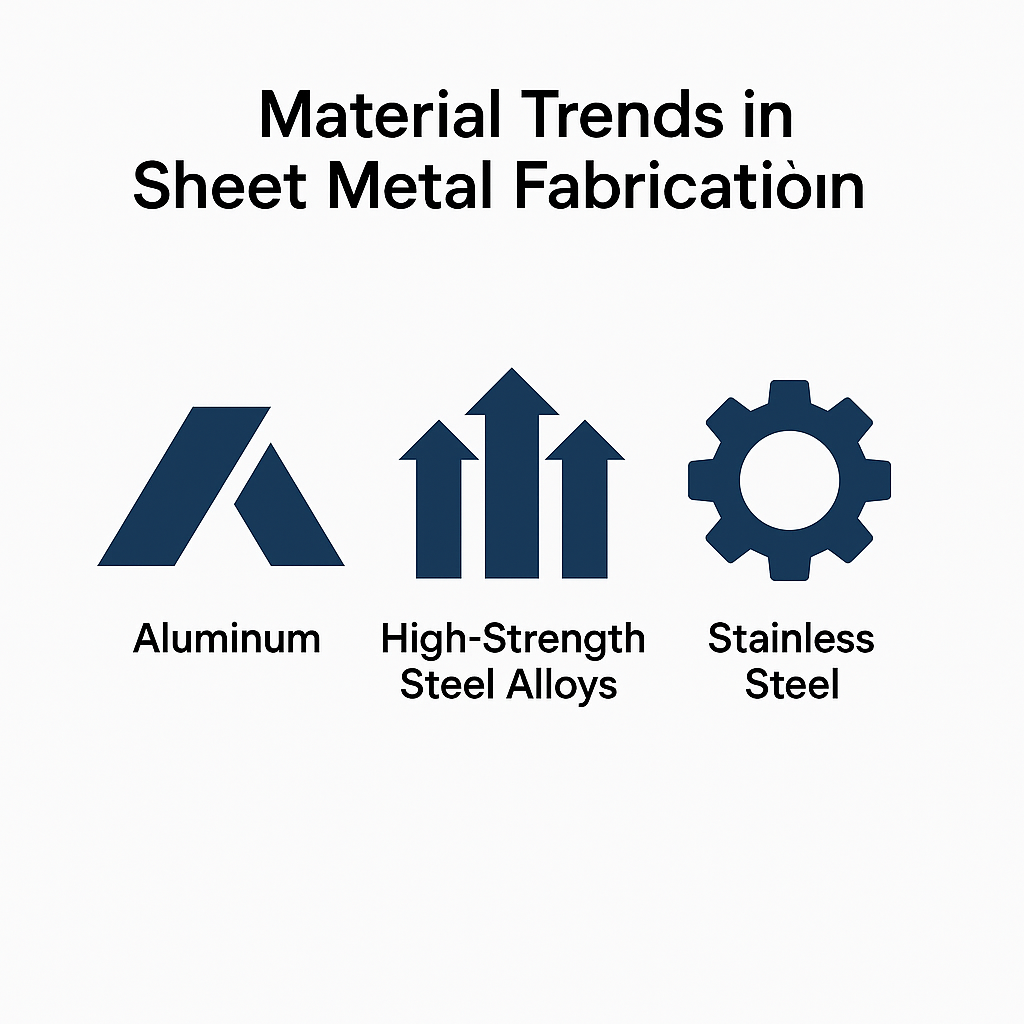

Aluminum: The Lightweighting Champion

Aluminum adoption keeps climbing in automotive, aerospace, and consumer electronics. Market data confirms aluminum demand is rising across multiple applications due to weight reduction priorities and corrosion resistance.

Working with aluminum requires different equipment and techniques than steel—which is why not every “full-service” fabricator can actually handle it at scale. Fabricating aluminum vs. steel involves different cutting parameters, forming considerations, and welding approaches.

High-Strength Steel Alloys: The Structural Backbone

High-strength and ultra-high-strength steels (AHSS/UHSS) continue to dominate automotive lightweighting and safety programs. These materials let engineers reduce weight while maintaining or improving crash performance—critical for EV range and occupant protection.

Processing AHSS requires understanding springback, forming limits, and how these alloys behave under laser cutting. It’s why design for manufacturability conversations matter early in the development cycle.

Stainless Steel: The Versatile Workhorse

Stainless steel demand stays steady across food processing, medical devices, chemical processing, architectural fabrication, and marine applications. It’s consistently rated as one of the most versatile materials in fabrication, handling corrosive environments that would destroy carbon steel.

Different stainless grades serve different purposes—304 for general corrosion resistance, 316 for marine and chemical exposure, 430 for magnetic applications. Knowing which grade solves your specific problem saves money and headaches.

Geographic Dynamics: Why Location Matters More Than Ever

The Nearshoring Reality

Nearshoring and reshoring accelerated through 2023–2024 and show no signs of slowing. While exact percentages vary by industry, multiple analyses confirm significant movement of supply chains into the U.S., Mexico, and Canada.

Mexico’s growth in automotive and electronics manufacturing strengthens demand for U.S. fabrication partners who can provide:

- Regional redundancy when a single facility creates supply chain risk

- Shorter lead times compared to overseas alternatives

- Cross-border logistics support for North American production networks

Multi-Location Advantages

Fabricators with multiple facilities across regions—like EVS Metal’s footprint in New Jersey, Pennsylvania, New Hampshire, and Texas—offer capabilities single-location shops can’t match:

- Capacity balancing when one facility hits constraints

- Lead-time optimization by routing work closer to your production line

- Disaster recovery and continuity when disruptions hit

- Customer proximity across different industries and geographic markets

This isn’t marketing speak—it’s operational reality. When an OEM in Texas needs faster delivery or a Northeast customer requires overflow capacity, multiple locations solve real problems that single-site fabricators can’t address.

Capabilities That Separate High-Performing Fabricators

If you’re evaluating fabrication partners in 2025, the baseline requirements have evolved. Buyers should prioritize:

Advanced equipment capabilities. Fiber lasers, robotic welding systems, multi-axis CNC machining, in-house powder coating—these determine what’s actually possible.

Scalability and capacity. Can your fabricator handle both prototype volumes and production runs? Do they have capacity headroom for when your forecasts increase?

Geographic reach. Single-location fabricators create supply chain concentration risk. Multi-facility partners provide flexibility.

Quality certifications. ISO 9001:2015, AS9100, and ITAR certifications signal process maturity and documentation rigor.

Engineering support. The best fabrication partners provide design for manufacturability feedback that reduces cost and improves quality before tooling starts.

Financial and operational stability. You’re not just buying parts—you’re entering a relationship that needs to last through product lifecycles.

These attributes separate top-performing fabrication suppliers from shops competing primarily on price.

The Sourcing Mistakes Buyers Still Make

Even experienced procurement teams fall into predictable traps when evaluating fabricators:

Optimizing for quoted price instead of total landed cost. The lowest quote rarely delivers the lowest total cost when you factor in rework, delays, expediting fees, and engineering time spent fixing manufacturability issues. Total landed cost tells the real story.

Ignoring geographic risk concentration. Single-location fabricators create supply chain vulnerabilities. Weather events, labor disruptions, or equipment failures can halt your entire supply. Multi-facility partners provide options when problems arise.

Assuming “full-service” means actual capability. Plenty of shops list capabilities they rarely execute or can’t scale. Ask about recent projects in your material, volume range, and tolerance requirements—then verify with references.

Underestimating lead time variability in tight markets. As capacity tightens across multiple industry segments simultaneously, fabricators with advanced equipment and certified processes will prioritize their strategic accounts. New buyers entering the queue may find extended lead times or limited availability.

Skipping the manufacturing review. The best fabrication partnerships start with design review conversations before tooling begins. Shops offering genuine design for manufacturability input will save you money and improve quality—but only if you engage them early.

Looking Forward: Durable Growth Drivers Through 2030

Updated 2025 forecasts point to several long-term growth drivers that aren’t dependent on economic cycles:

- Continued EV adoption → sustained growth in battery housings, thermal management plates, structural modules

- Federal infrastructure spending → predictable demand for HVAC components, architectural metals, utility enclosures

- Electronics proliferation → more sophisticated enclosures in vehicles, buildings, industrial systems

- Reshoring momentum → increased domestic fabrication partnerships as companies reduce overseas dependency

- Sustainability and energy efficiency → competitive differentiators in sourcing decisions, not just nice-to-haves

Fabricators investing in automation, advanced materials processing, and regional coverage will capture disproportionate share of this demand. Those standing still will find themselves competing in shrinking commodity segments.

EVS Metal: Capabilities Aligned with Market Demand

EVS Metal’s investments over the past several years—advanced fiber lasers, robotic bending and welding, horizontal machining centers, comprehensive powder coating, and rigorous quality systems—align with the industry’s highest-growth segments.

Our four facilities spanning New Jersey, Pennsylvania, New Hampshire, and Texas support:

- Regional redundancy for supply chain resilience

- Faster lead times through proximity to customer operations

- Diverse industry expertise across automotive, aerospace, electronics, construction, and medical devices

- Consistent ISO 9001:2015 certified processes across all locations

This geographic and technical positioning matches the key market demand drivers emerging in 2025—and positions us to grow alongside customers navigating this industry evolution.

Whether you’re launching EV programs, expanding infrastructure projects, or building out electronics manufacturing, the fabrication partner you choose now will shape your competitiveness for years to come.

Frequently Asked Questions

What is driving sheet metal fabrication demand in 2025?

Sheet metal fabrication demand in 2025 is driven by electric vehicle manufacturing, federal infrastructure spending, widespread reshoring, and increasing automation across multiple industries. These factors are creating sustained long-term growth for advanced fabrication services.

How fast is the sheet metal fabrication market growing?

Recent forecasts place the sheet metal fabrication services market at $17–22 billion today with projected growth to $30–33 billion by the early 2030s. The North American fabrication equipment market is also expanding at a compound annual growth rate of approximately 6.4% through 2030.

Which industries are creating the most demand for fabrication services?

Automotive and electric vehicles, aerospace and defense, construction and infrastructure, and electronics and telecommunications are the primary sectors driving fabrication demand in 2025. Each of these industries depends heavily on precision metal components and assemblies.

What materials are trending in advanced sheet metal fabrication?

Aluminum usage continues to rise due to lightweighting requirements in automotive, aerospace, and electronics. High-strength steel alloys such as AHSS and UHSS are expanding in automotive applications, while stainless steel remains essential across food processing, medical devices, architecture, and marine environments.

Why does fabrication location matter in today’s supply chain?

Location affects lead times, logistics costs, and supply chain risk. Nearshoring and reshoring trends have increased the importance of working with fabrication partners who operate multiple U.S. facilities, enabling faster delivery, redundancy, and regional capacity balancing.

What capabilities separate high-performing fabricators from commodity suppliers?

Top-performing fabricators offer advanced equipment such as fiber lasers and robotic welding, multi-location scalability, ISO-certified quality systems, engineering support for manufacturability, and operational stability. These capabilities reduce risk and improve part quality and delivery performance.

What sourcing mistakes do buyers commonly make when selecting fabrication partners?

Common sourcing mistakes include optimizing only for quoted price instead of total landed cost, relying on single-location suppliers, assuming advertised capabilities match real capacity, underestimating lead time volatility, and skipping early design-for-manufacturability reviews.